Check Point SoftwCheck Point Software (CHKP): The Ultimate Cyber Security Compounder

Welcome back to another deep-dive analysis. Today, we are putting Check Point Software Technologies (NASDAQ: CHKP) under the microscope. In a cyber security sector obsessed with hyper-growth, cash-burning upstarts, Check Point is a refreshing anomaly.

After reviewing a decade of the company's financial realities—from their 2016 annual reports through the newly released Q4 2025 results—one thing is crystal clear:Check Point is not a value trap, nor is it a turnaround. It is the ultimate "Compounder."

Here is why I am issuing aBUYrating for long-term, value-conscious investors.

1. The "Quality" Test: A Masterclass in Margin and Recurring Revenue

Check Point has successfully executed one of the hardest maneuvers in legacy tech: pivoting from hardware/licenses to a recurring subscription model without destroying profitability.

The numbers speak for themselves. Back in 2016, the company generated $1.74 billion in total revenues, with legacy products and licenses bringing in $573 million compared to just $390 million for security subscriptions [1]. Fast forward to full-year 2025, and that mix has completely flipped [2, 3].Total revenues hit $2.73 billion in 2025, with security subscriptions surging 10% year-over-year to a massive $1.22 billion[3].

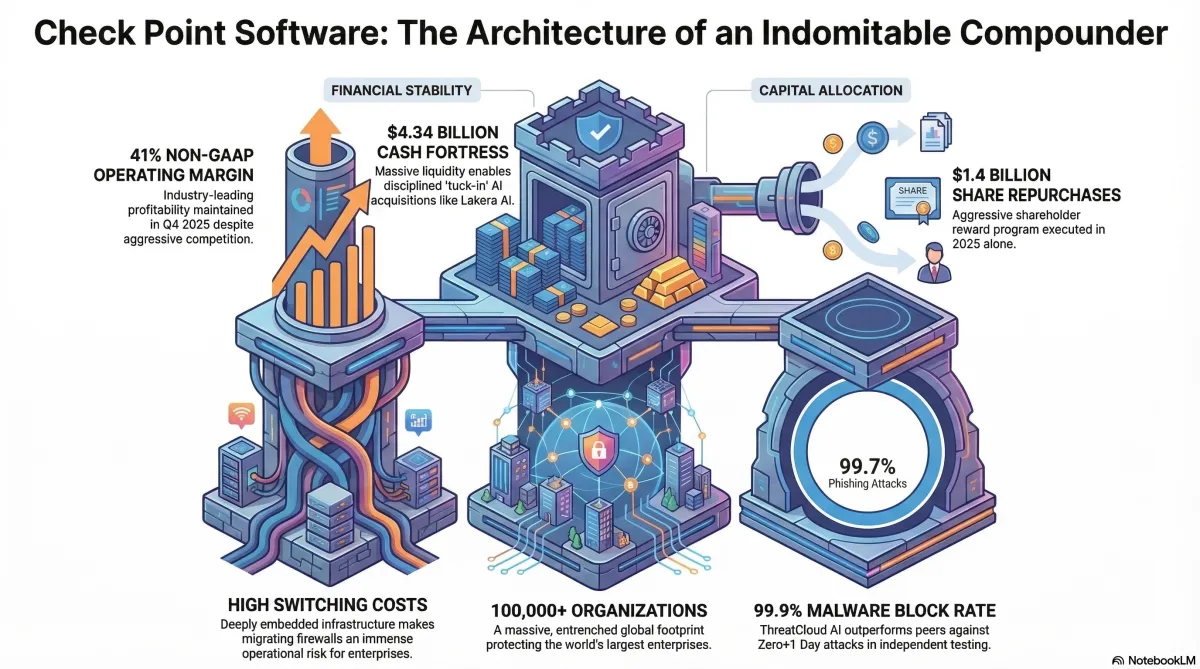

Furthermore, this growth is highly profitable. In the fourth quarter of 2025, Check Point posted an impressive Non-GAAP operating margin of 41% [2]. This pristine profitability translates directly to the bottom line, withGAAP Earnings Per Share (EPS) growing 29% year-over-year to $9.62 in 2025, while Non-GAAP EPS hit $11.89[3].

2. The Narrative: AI, Cloud, and a Historic Leadership Handoff

Strategically, Check Point has evolved from being the inventor of the stateful inspection firewall into a comprehensive, AI-powered platform [4]. They consolidate their offerings under the "Infinity" architecture, covering network (Quantum), cloud (CloudGuard), and workspace (Harmony) security [5].

Late 2024 marked the end of an era aslegendary founder Gil Shwed transitioned to Executive Chair, passing the CEO baton to Nadav Zafrir[6, 7]. Zafrir’s mandate for 2026 and beyond is crystal clear: secure the enterprise AI transformation [3].

Instead of chasing dilutive mega-mergers, management has historically relied on highly disciplined, capability-expanding "tuck-in" acquisitions. Notable integrations include Dome9 for cloud security in 2018 [8, 9], Avanan for cloud email in 2021 [10, 11], Perimeter 81 for zero-trust access in 2023 [12, 13], and Cyberint for external risk management in 2024 [14]. Most recently,Check Point closed the $190 million acquisition of Lakera AI in Q4 2025 and announced three new Q1 2026 acquisitions (Cyata, Cyclops, and Rotate) to aggressively expand its AI security and exposure management footprint[3, 15, 16].

3. The Competitive Moat

The cyber security landscape is fiercely competitive, with heavyweights like Palo Alto Networks, Fortinet, and Cisco fighting for enterprise budgets [17].

Check Point defends its moat with an installed base of over 100,000 organizations and industry-leading efficacy [4]. Independent testing by Miercom routinely validates Check Point's superiority; recent benchmark tests showed the company achieving a99.9% malware block rate against Zero+1 Day attacksand a 99.7% block rate against phishing attacks [14]. When you combine this best-in-class threat prevention with the high switching costs of ripping out core enterprise firewalls, you get a remarkably sticky customer base.

4. Headwinds and Tailwinds

The Tailwinds:The shift toward hybrid cloud environments, coupled with AI-fueled threat complexity, provides a massive secular growth runway [5]. Check Point's newly acquired AI security stack perfectly positions them to monetize the enterprise AI boom [3].

The Headwinds:Check Point is headquartered in Tel Aviv, Israel, exposing it to severe geopolitical risks from the ongoing war and hostilities involving Hamas, Hezbollah, Iran, and Yemen [18]. Furthermore, the company faces intense wage inflation and competition for top-tier R&D talent [19].

5. Capital Allocation: The Ultimate Buyback Machine

If you want to know how management treats shareholders, look at their capital allocation. Check Point is a relentless cannibal of its own shares.

In 2025 alone, the company spent approximately $1.4 billion to repurchase 6.8 million shares[20]. Over the last decade, these systematic buybacks have drastically reduced the outstanding share count, artificially supercharging EPS growth even when top-line growth has been in the mid-single digits.

Financially, the company operates from a fortress balance sheet. They ended 2025 with$4.34 billion in cash, marketable securities, and short-term deposits, which was significantly bolstered by a recent $2 billion convertible senior notes offering [16]. In 2025, they generated a massive $1.23 billion in operating cash flow [20].

The Final Verdict: BUY

Check Point (CHKP) is a quintessential Compounder.

It provides an unparalleled margin of safety through its $4.34 billion cash pile, >40% Non-GAAP operating margins, and aggressive share repurchases [2, 16]. While it lacks the dizzying revenue growth of cloud-native disruptors, the recent injection of new CEO Nadav Zafrir and a flurry of AI-focused acquisitions represent a tangible catalyst for accelerated commercial execution in 2026 [3].

For investors seeking sleep-well-at-night exposure to the booming cyber security sector, Check Point is a definitiveBuy.

--------------------------------------------------------------------------------

Disclaimer: This article is for informational purposes only and does not constitute financial advice. Please do your own due diligence before making any investment decisions.